A RIN is a tax and a subsidy that forces renewables into fuel – Part 2, the RIN subsidy

Summary

This is a four-part blog series describing the renewable identification number (RIN) as a tax (part 1) and a subsidy (this part 2) that forces renewables into fuels (part 3), and how this tax-and-subsidize interpretation resolves the apparent contradiction (part 4) at the core of the legal dispute over RINs now in its 10th year. The RIN tax increases the blend cost of refined blendstocks and the RIN subsidy reduces the blend cost of renewable blendstocks. These changes cause the demand for refined blendstocks to decrease and the demand for renewable blendstocks to increase. In the case of the 10% ethanol/gasoline blend sold to consumers, which we are using as an example case, the price of the blended fuel is almost exactly unchanged. The payment of the RIN tax by refiners and the receipt of the RIN subsidy by blenders are tangible transactions whose financial effects are easy to measure and easy to understand. But two other financial effects are intangible, not easy to measure, and not easy to understand – they are the effects on the market prices of the refined blendstock (called BOB) and the blended fuel (called E10). A key for understanding RINs is to recognize that, in competitive markets, these two market prices emerge “automatically” as a consequence of competitive forces in the market rather than by the deliberate action of any individual or single company. Another key is to recognize how competition in the E10 market forces the blender to apply the revenue from its RIN sale as a credit on the effective blend cost of ethanol, and how that causes the RIN tax to cross-subsidize ethanol used as fuel. At the individual refiner and blender level, the RIN has no impact on profitability. At the aggregate market level, there are impacts on the refining and blending industries that requires a different, related analysis. This tax-and-subsidize interpretation provides a sound fundamental framework for making sense of the apparent contradiction at the core of the 9-year dispute over RINs, and for understanding other important subjects like RIN pricing theory.

A RIN is a tax and a subsidy that forces renewables into fuel – Part 2, the RIN subsidy

Each quarter, public companies report their firm’s earnings and take questions from analysts in earnings conference calls. Since 2013, no single topic has caused more angst in refiners’ earnings conference calls than RINs (Renewable Identification Numbers). RINs are a feature of the Renewable Fuel Standard (RFS) which requires renewables like ethanol and bio-based diesel to be blended into fuels sold in the USA. In this series we are digging into the fundamental aspects of RINs which are at the root of this long-running controversy.

We are examining this definition of a RIN:

A RIN is a tax and a subsidy that forces renewables into fuels.

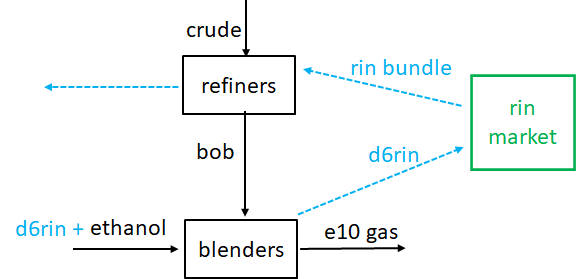

Part 1 described how the RINs system requires refiners to acquire and retire a rin bundle for each gallon of fuel they sell into the US market. That is like a tax on sale of refined fuel blendstocks and is depicted in the top half of Figure 1, revolving around the refiner.

How does this “rin tax” affect a refiner’s profit? There are 2 camps. Camp A says it hurts a refiner’s profit and Camp B says it doesn’t. Their disagreement hinges on one key question — whether the cost of the RIN tax is passed through to downstream blenders in a higher price for the bob the refiner sells to the blender.

The disagreement about the RIN tax is one root of the controversy. Now we move on to consider the rin’s unsung role as a subsidy, which is depicted in the bottom half of Figure 1 and revolves around the blender.

The example we are considering is the blending of 10% ethanol into refined gasoline to produce the e10 gasoline we pump into our cars, SUVs and pickups. The refined gasoline blendstock used for this is called blendstock for oxygenate blending (bob).

One gold nugget per gallon of ethanol

By rule, every gallon of ethanol contains an incentive to blend that gallon into fuel. We can think of it as a nugget of gold that can only be released by blending that gallon into fuel. A nugget in any gallon not blended to fuel remains trapped there. The nugget is called an “attached RIN”. Call that the RIN subsidy, which is a negative tax. In our example, it is a d6 RIN, the code d6 referring to ethanol; that is, the d6 RIN is the category of RIN that comes attached to a gallon of ethanol.

The blender buys the gallon of ethanol and blends it with purchased bob, whereupon he captures the nugget as a “separated d6 RIN” and sells it into the RIN market for cash.

What a deal! That sounds like a windfall for the blender.

And that is the second root of the controversy. Is it really a windfall for the blender? There are two camps. One says it is and one says it isn’t.

Is the RIN subsidy a windfall for blenders?

The RINs literature is full of references to $100 million RIN windfalls for blenders. For example, Carl Icahn’s said, in his 2016 letter to EPA: “. . . companies are actually boasting about the windfall profits they are receiving as a result of the EPA’s irrational rulemaking. One of the biggest known beneficiaries of the over-priced RIN market is Murphy USA, a large gasoline chain owner and blender that collects RINs and sells them at a huge profit. In its 2015 10-K, it boasted that it made $117.5 million selling RINs to obligated parties in 2015.”

Carl Icahn was right. In 2016, Murphy, and other blenders and retailers were heartily slapping each other on the backs while smoking expensive cigars, congratulating themselves on their brilliance in cranking out profits with RINs.

In 2016, Casey’s General Stores, a large gasoline chain owner and blender, was among those treating RIN sales as an add-on to fuel margin. In their quarterly earnings press releases, there was a boilerplate paragraph reporting RIN revenue as extra profit margin. The paragraph was included each quarter, and the boost in fuel margin was celebrated in conference calls. For example, in 1st quarter 2016: “During this time we sold approximately 15.7 million renewable energy credits, commonly known as RINs at an average price of $0.51. This represented about $0.016 per gallon benefit to the fuel margin”. And in 2nd quarter 2016, “During the quarter, we sold 13.6 million RINs for $4.7 million. This represented about $0.01 per gallon improvement to the fuel margin” — and so on, each quarter.

Casey does an about-face

But then in 2018, Casey’s suddenly did an about-face. They recognized RIN revenue was coupled to a less tangible, passed through, higher cost of BOB, and hence it did not in fact increase their fuel profit margin. In the 4th quarter 2018 earnings conference call, analyst Damian Witkowski asked Casey’s Management: “then RINs were about $7 million contributor last year, I don’t see anything in the press release, how much were they this year?”, and William J. Walljasper, Casey’s Chief Financial Officer responded: “ . . . so just to be clear, I’ll give you that number then I have a clarifying commentary. In Q4 we sold about 14.8 million RINs for a value of just under $8 million in the fourth quarter. But I will say this, that I think we mentioned — might have mentioned this in the last conference call that

“we believe RINs are embedded in the cost of the product. And so when RINs move up and down there is adjusting movements in the wholesale cost”

William J Walljasper, CFO, Casey’s General Stores

“we believe RINs are embedded in the cost of the product. And so when RINs move up and down there is adjusting movements in the wholesale cost” (NOTE – the reference to “wholesale cost” refers to the price they pay for BOB).

This was a striking change in how Casey’s reported fuel profit margins. Later in the same conference call, in response to another analyst’s question on the matter, Walljasper elaborated:

I think RINs tends to be somewhat of a misunderstood anomaly in the market.

William J Walljasper, CFO, Casey’s General Stores

I think RINs tends to be somewhat of a misunderstood anomaly in the market. I mean we don’t necessarily believe that RINs, I will put it this way Bonnie, some of our highest fuel margin quarters we had some of the lowest RIN contribution and so we do believe there is an offset to the wholesale, as RINs come down it will be a corresponding offset in the wholesale.”

Walljasper was stating the pass-through theory. The RIN cost gets “passed through” by refiners and “picked up” by blenders. Casey’s financial analysis showed, on further review, their RIN revenues were not adding to profit but merely offsetting corresponding increases in what they were paying for BOB.

In the 4th quarter of 2019, Walljasper was still trying to wean financial analysts off the notion RINs were a profit stream, saying “Terry is exactly correct. We believe RINs are embedded in the cost and so the ebb and flow of that gets kind of flushed out overall in the margin.”

So we see, in late 2019, 12 years after the RIN system took hold, refiners, blenders, retailers and financial analysts were all still struggling to come to grips with this confounding RIN and its impact on their profits.

Two sides of the same coin

The Casey’s story bears a family resemblance to the story told about refiners in part 1 of this series. For both refiner and blender, the RIN has a tangible part about cash going out or coming in the door, and an intangible part about how the market price for BOB is different from what it would otherwise have been.

The family resemblance exists because we are examining two sides of the same coin. The RIN is, at once, both a tax and a subsidy. The refiner sees a tangible tax in cash paid out for the RIN and an intangible increase in the price he receives for BOB. The blender sees a tangible subsidy in cash received for the RIN and an intangible increase in the price he pays for BOB. The changing price of BOB is the intangible part that connects the two tangible parts and clouds understanding of the impact on profits.

An essential point is that the price of BOB is a market price. No one turns a knob that directly sets it; instead it emerges from the collective actions of all market participants as they make their individual decisions each day. That’s why its role is less intuitive, and why the pass-through theory has caused seemingly never-ending disagreements.

Or are they misunderstandings?

Pass-through or no pass-through?

Having described both the tax and subsidy side of the RIN, we will consider now two cases: 1) If we assume the RIN pass-through theory is true, then the picture is the refiner’s RIN cost is being offset by the refiner passing through the RIN tax to the blender, and the blender’s RIN revenue is being offset by the blender “picking up” the RIN tax from the refiner; and this transfer of RIN cost from refiner to blender is being accomplished by a change in the market price of BOB which occurs automatically through the workings of the law of supply and demand in the competitive BOB market, and this leaves both refiner and blender more-or-less even when the dust settles. 2) If we assume the RIN pass-through theory is false, the picture is blenders are reaping an unearned RIN windfall funded by an unfair RIN tax on refiners while the BOB price is static, unaffected by all the pulling and tugging going on around it, unchanged from where it would otherwise have been.

The disagreement is still resolved and we are told litigation will continue, though over time, the pass-through theory has been gaining acceptance in blenders’ and refiners’ views (the financial analysts still seem confused).

Forcing ethanol into fuel

If the RIN gold nugget is not a windfall, then what is it? We have a clue: Someone has devised a scheme that plants a prize, like a gold nugget, into ethanol that can only be captured by blending that ethanol into gasoline. That sounds suspiciously like a tactic to force ethanol into fuel.

Recommendation

Anyone with a stake in RINs pricing and economics should get Hoekstra Research Report 10 which includes the Hoekstra ATTRACTOR spreadsheet spreadsheet that accurately calculates D4T, the theoretical RIN price, tracks it versus quoted market prices, and predicts how RIN prices will change with the variables that affect them. Why not send a purchase order today?

George Hoekstra george.hoekstra@hoekstratrading.com +1 630 330-8159

Anyone with a stake in RINs pricing and economics should get Hoekstra Research Report 10

The next step

The next step is to answer two more questions: How exactly do RINs force ethanol into fuels? – and how does this two-pronged tax-and-subsidize scheme affect the price consumers pay for fuel at the pump?

The next step is to answer two more questions: How exactly do RINs force ethanol into fuels? – and how does this two-pronged tax-and-subsidize scheme affect the price consumers pay for fuel at the pump?

These questions are addressed in part 3 of this series.

George Hoekstra george.hoekstra@hoekstratrading.com +1 630 330-8159