Update on the MPC-PSX stock price spread

Throughout 2021 and 2022, I have been tracking the difference in performance of Marathon Petroleum (MPC, green) and Phillips 66 (PSX, red) stock.

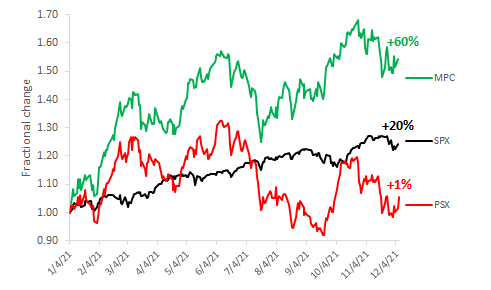

The first blog post, from Dec 8, 2021, showed the difference being 60% gain for MPC versus 1% gain for PSX. The S&P 500 index is shown for reference:

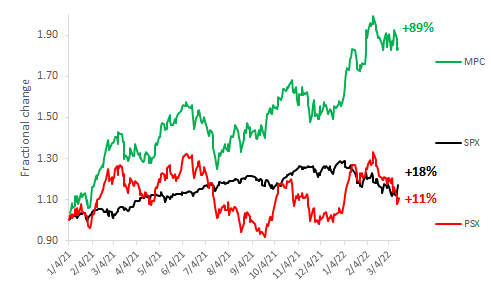

Now, 100 days later, the gap has grown, reaching a 78% difference since the first trading day of 2021:

It is hard to find any time interval since the beginning of 2021 you wouldn’t have made good money buying MPC and selling PSX.

One look at the chart suggests something has been dragging down PSX stock. My theory is their refineries are bottlenecked by difficulties making the ultra-low sulfur, high octane blend stocks needed to meet the Tier 3 clean gasoline specification that kicked in at the beginning of 2021. In that situation, refiners can go in the market and buy those barrels instead of making them in their refineries, which is a convenient solution, but it cuts their gasoline margin by a factor of five. It effectively papers over a fundamental weakness that will continue to drag down refining margin and the stock until something is done.

Refiners like Marathon, who are better-equipped to make additional Tier 3 gasoline at low incremental cost, are beneficiaries of that foregone margin.

That’s my unpopular, contrarian theory which is detailed throughout this blog and in many of my industry presentations, reports, and other publications.

As an incidental point, MPC closed today at $77.15 and and PSX at $77.55, so we are near a threshold where the prices will cross. On the first trading day of 2021, the prices were MPC $40.75, PSX $69.88.

Conclusions

- Phillips 66 is among a group of refiners whose stock performance is being hurt by difficulty meeting the new Tier 3 clean gasoline specification.

- Marathon, by contrast, is in a group whose refineries are well-equipped to make Tier 3 clean gasoline.

- Since Tier 3 is here to stay, we should expect divergence of financial results to continue until more red refineries either take corrective action or go bust.

Recommendation

There are steps any refiner can take to immediately improve Tier 3 gasoline profitability. There are many more things they could do in the near-term to turn Tier 3 from a problem into a profit opportunity. Refiners affected by Tier 3 should buy the Hoekstra Research Report 8 and use it to help take a fresh look at their Tier 3 strategy. The cost is negligible. For a typical refiner, it costs only 1 minute’s worth of your annual revenue to confront and get your arms around this important, overlooked Tier 3 issue.

Hoekstra Research Report 8

Our three-year multi-client research project measured the effects of making Tier 3 gasoline in pilot plant and commercial performance tests. We developed new methods and tools that are helping our clients optimize performance of gasoline desulfurizers to avoid hidden hits to margin capture and adopt profitable sulfur credit strategies. All our data and tools are available to anyone for immediate application at negligible cost. Please see this offer letter and join our client group today: Hoekstra-Trading-Offer-letter-Research-Report-8-refiners-under-1-MBD