The Big Bang Theory Part 2 – Could there be more RIN price explosions?

See Part 1 of this series

In 2013, the price of the D6 Renewable Identification Number (RIN) spiked from a low of one cent in 2012 to over one dollar per RIN in July 2013. It is hard to find such a spectacular price move in the history of major commodity trading. RINs are credits used to certify compliance with the Renewable Fuel Standard (RFS) which requires certain minimum volumes of biofuels to be blended into fuels sold in the United States. The 100-fold (=10,000%) move in the D6 RIN meant U.S. refiners and importers, who tend to be short RINs, were suddenly facing RIN costs of $14 billion per year.

The root cause of this price explosion was the government mandate that 13.8 billion gallons of ethanol must be used in gasoline when only 13.0 billion gallons could possibly fit into the gasoline being consumed in the United States (see Big Bang part 1). It was like when you pour cream into your coffee until it reaches the brim, no more would fit.

RIN credits come in different categories. The D6 RIN applies to the blending of corn-derived ethanol into the gasoline used in cars, SUV’s and pickups. Another category, code named D4, applies to the blending of soybean-derived biofuel into the diesel fuel used by truckers.

The RIN credit system is important, complex and confusing. Because of its importance to those in the energy industry, it is worth the effort to understand it thoroughly at a fundamental level. Our recent Misunderstanding series covered RIN fundamentals, focusing on the D6 RIN as a tax and a subsidy that forces renewables into fuels. Today’s blog uses the story of the 2013 D6 “Big Bang” price explosion as a starting point to explain the fundamental mechanism that determines RIN prices.

In 2012, everyone was aware of the dilemma caused by a 13.8 billion gallon minimum and a 13.0 billion gallon maximum. There were three possible solutions. They were: 1) the E85 solution, 2) the legal solution and 3) the biodiesel solution. The biodiesel solution is what solved the problem. It did so by stimulating the generation of additional gallons of biodiesel which, by RIN rules, counted toward meeting the ethanol quota.

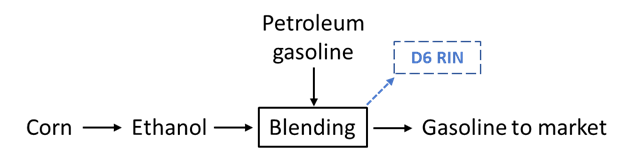

As explained in Misunderstanding Part 3 – Do RINs Increase the Price of Gasoline to Consumers?, a D6 RIN is earned when you blend corn-based ethanol into gasoline as shown in Figure 1.

Figure 1 D6 production pathway

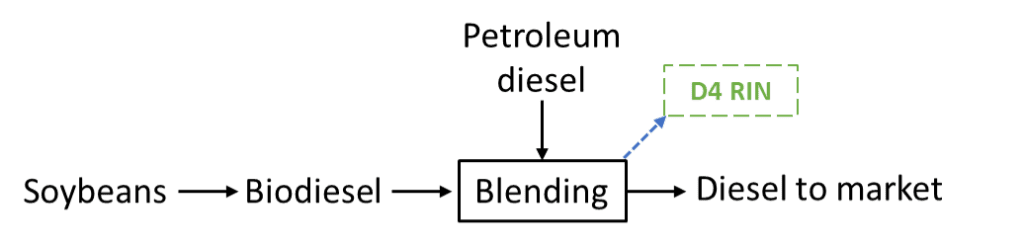

Similarly, a D4 RIN is earned when you blend soybean-derived biodiesel into the diesel fuel used by truckers. The flow chart for that production pathway is Figure 2.

Figure 2 D4 production pathway

The blender buys soybean-derived “biodiesel” and blends it with refined petroleum diesel to produce the blended diesel fuel for truckers.

For a quick digression into the world of chemistry, think for a moment of soybean oil as a 3-legged stool. If you (chemically) chop the legs off the stool, the legs make perfectly good diesel fuel. That is what biodiesel producers do. They chemically chop the legs off soybean oil molecules (called triglycerides) to make three molecules of diesel fuel (called bio-based diesel, or biodiesel for short), and some byproducts. It’s about that simple.

Returning now to flow diagrams and economics — it costs much more to make diesel fuel by chopping the legs off soybean oil then it does to boil it out of crude oil you pump out of the ground.

For example, on February 1st, 2013, the price of biodiesel was $4.45 per gallon and the price of blended product diesel sold to truckers was $3.18 per gallon. The biodiesel producer will not produce the gallon of biodiesel without being paid at least $4.45 and the fuel blender will not pay any more than the $3.18 he can get by selling the blended fuel. We have another dilemma here where the maximum price is below the minimum. A biodiesel subsidy is needed to make things work. It is provided by the D4 RIN which, by design of the RIN system, is placed like a virtual gold nugget into each gallon of biodiesel and then cashed out by the blender when that biodiesel gallon is blended into the product diesel.

If you pause and think about this, you will see, for this to work, the value of the D4 RIN must be just enough to cover the difference in the prices of biodiesel and diesel. At that price, both the biodiesel producer and blender can break even. And the refiner, who is obligated to buy the RIN under threat of big fines, will bid up the RIN price to just that level at which the extra gallon and its RIN will be produced. That is the fundamental mechanism that determines the D4 RIN price.

To recap, when the D4 RIN price is bid up to the difference between the prices of biodiesel and diesel, an additional gallon of biodiesel and its D4 RIN will be produced and blended; and the refiner’s obligation to buy the RIN ensures the price will be bid up to that level, thus forcing the mandated quantity of renewables into fuel.

This principle is used to quantify and accurately model the RIN price, but there are several caveats. First, by rule, one gallon of biodiesel produces not just 1, but 1.5 D4 RINs. Second, biodiesel delivers less energy per gallon than refined petroleum diesel. Third, other subsidies like the biodiesel tax credit play into the producers’ and blenders’ breakeven prices. Fourth, known or expected future events, like changes in mandates or tax credits, will affect today’s price. All of these can be accommodated in a pricing model using the fundamental equation defined by the mechanism described above.

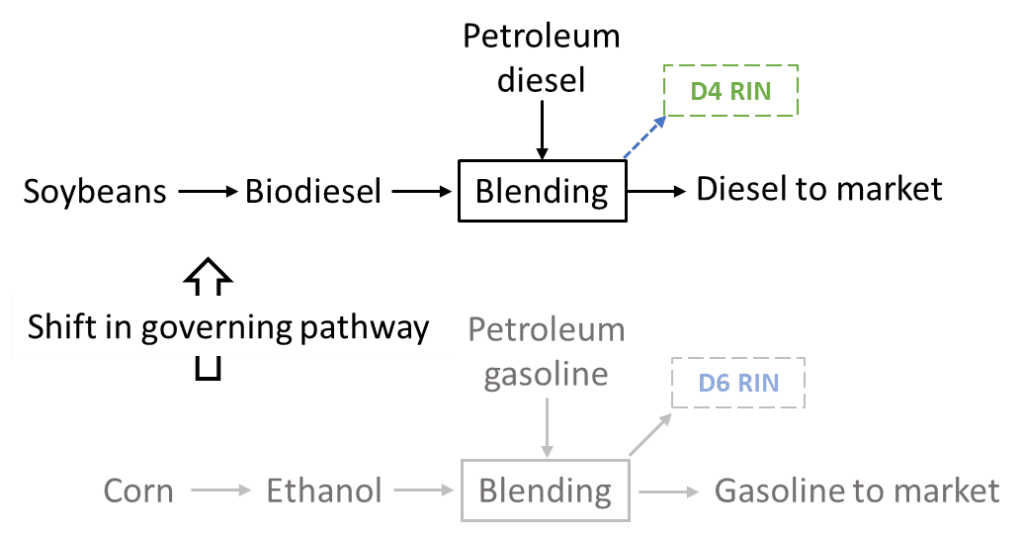

Figure 3 shows the flow diagram for D4 RINs above that for D6 RINs, and the transition from one to the other that occurred at the Big Bang.

Figure 3 Transition in governing pathway from D6 to D4 pathway

The Big Bang happened when the mandated quantity of D6 RINs first exceeded the maximum capacity for blending ethanol into gasoline. At that point, the requirement to produce 0.8 billion more D6 RINs drove the D6 RIN price up to the point where it subsidized the blending of more biodiesel gallons which generated more D4 RINs which then substituted for D6s to make up the shortage of D6 RINs. In terms of the flow diagrams, there was a step transition where the production of D6 RINs started occurring by the D4 pathway.

This transition was designed into the RIN system by a feature called the “nesting” of RIN categories, by which some kinds of RINs can substitute for others. In 2012, it was clear to those with fundamental understanding that the biodiesel solution was imminent and that it would blow the lid off the D6 price.

Why weren’t refiners, who naturally tend to be short RINs, buying D6 RINs by the truckload in 2012, when everyone saw the D6 supply/demand dilemma coming, and people knew the biodiesel solution would kick in like a relief valve, driving the D6 RIN price up to the D4? The most likely explanation is that big RIN stakeholders lacked a fundamental understanding of the workings of the complex RIN credit system. In particular, they did not foresee how the D4-D6 nesting feature would (by design) cause a big step increase in the D6 price up to the D4 price.

The RIN credit system is indeed complex, but nowhere near as complex as refineries themselves, or the systems used to operate and optimize them, or the tax codes that affect their profitability. By all accounts, RINs are here to stay. Any entity with a stake in RINs should become fully proficient in their details, as they are in other critical aspects affecting profitability.

Could something like the Big Bang happen again? Our answer is yes. On the list of known and possible coming changes are the growth of renewable diesel production, multi-year standards, sustainable aviation fuel (SAF), bio intermediates, new auditing requirements, the biodiesel tax credit, and the Section 45Z clean fuels production credit. How well have big RIN stakeholders anticipated the RIN price implications of these coming changes? Until they have a firm grip on RIN price fundamentals, there is a risk of people again “getting caught with their shorts showing”.

Recommendation

Those who have an interest in RIN pricing should get Hoekstra Research Report 10 and the ATTRACTOR spreadsheet which calculates D4T, the world’s first licensed environmental credit, compares it to market quotes, and enables informed analysis and forecasting of RIN prices.