Time to regroup on RINs

The refining industry has little to show for its investment in the 8-year battle to get relief on RIN costs. Though Big Oil is my career home, and refiners are my prime target customers, I must admit we seem over matched in this battle.

It’s a familiar feeling for a fan of the Chicago Bears, who suffered 9 sacks and produced a grand total 47 yards offense against the Browns yesterday.

I will go a step further and say it’s time for refiners to regroup and consider why we keep losing these RIN battles.

I have come to believe the refining industry has a competitive weakness in our understanding of the details of how RINs work and how their costs work through the supply chain. Yesterday someone asked me for specific evidence for this claim and I cited three research studies that came immediately to mind:

1) “Economic Impacts Resulting from Implementation of RFS2 Program”, study by NERA Economic Consulting for API, October 2012

This 2012 study, done for API, forecast that:

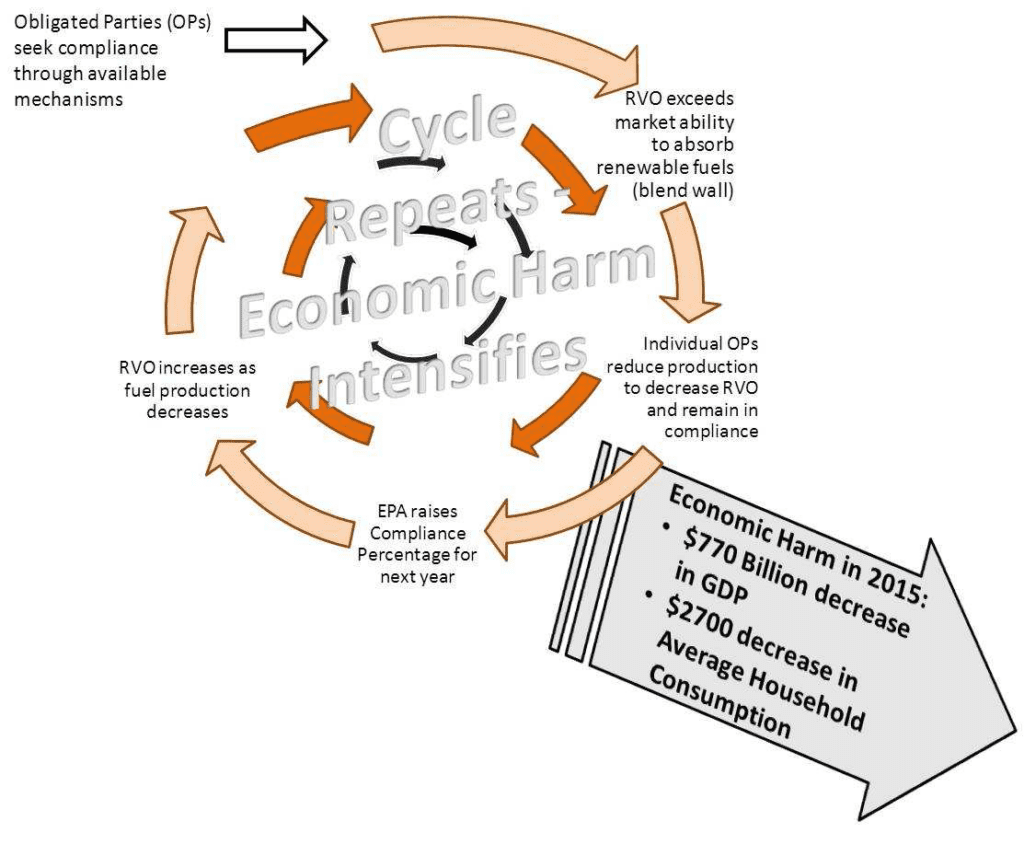

“As domestic fuel supplies decrease, large increases in transportation fuel costs would ripple through the economy imposing significant costs on society. More specifically, as the RFS2 mandate is ratcheted up every year, the fuels market will be pushed into a death spiral shown in Figure 1. The death spiral depicts the economic harm that occurs as individual obligated parties act to remain in compliance with the program.”

Excerpt from Executive Summary of “Economic Impacts Resulting from Implementation of RFS2 Program”

Figure 1: Economic Impact of Hitting the RFS2 Blend Wall: The Death Spiral

This forecast turned out to be wrong. A good question is, why did the authors not anticipate the use of biomass-based diesel to meet the conventional mandate? That was an expected solution to the blend wall problem that was anticipated by many others outside our industry, and it occurred as designed, avoiding the death spiral.

2) Charles River Associates paper “Ethanol RIN Waiver Credits”, Mar 9, 2018

This 2018 paper essentially argued for a price cap on RINs. It incorrectly assumed the biodiesel solution to the blend wall issue was unintended:

“Instead, the RIN deficiency has been met by expanding biodiesel consumption, based on an unintended result of the fuel-type nesting structure of the RFS.”

Excerpt from Executive Summary of “Ethanol RIN Waiver Credits”

Expanding biodiesel consumption was not an unintended result. In fact, that expansion occurred exactly as it was designed into the fuel-type nesting structure of the RFS.

This paper was also convincingly criticized by agricultural economist Scott Irwin of University of Illinois for, among other things:

“The report is disingenuous in the extreme regarding “compliance costs.” They focus almost exclusively on the initial cash expenditures of refiners for RINs. THIS IS NOT THE NET ECONOMIC COST OF COMPLIANCE FOR REFINERS.”

Scott Irwin, University of Illinois, on Twitter, Mar 9, 2018

and for mostly ignoring the reality of RIN cost pass through:

“So, yes they do mention pass through in the report but in an oblique footnote (irony alert: does that sound like anything else we have heard about recently?) The key is that you cannot understand true economic compliance cost of RFS without pass through”

Scott Irwin, University of Illinois, on Twitter, Mar 9, 2018

The paper was easily criticized — Scott Irwin’s critique came out the same day it was issued. A good question is, would it have survived a screening by knowledgeable people who really understood RIN fundamentals?

3) “Analysis of the RFS Program and the 2019 Proposed Standards”, by Craig Pirrong

This study was central in a 2021 court opinion that rejected refiners’ latest challenge to the 2019 RFS mandates. Upon reading it, I saw a critical flaw, as written in a previous post on this blog:

“Which leads me back to Friday’s court opinion rejecting refiners’ latest challenge to the 2019 mandates. That challenge was based on an academic paper that contradicts the pass-through theory. Having studied the paper, I conclude it suffers from the three pitfalls listed above, that is, it inadequately differentiates between the categories of fuels, RINs, and markets, which leads to wrong conclusions about how RINs affect prices and profits. For example, here are three key sentences from the paper, with my edits in red:

‘Note that the quantity of production and consumption of BOB declines.’

‘PR is the price that

consumersblenders pay’‘A positive D6 RIN price increases the price that

George Hoekstra in blog post “Refiners rebuffed again on RIN price pass through”, July 19, 2021consumersblenders pay forfuelBOB.'”

Without properly differentiating the fuel components and their positions in the process chain, the economic analysis is critically oversimplified and leads to wrong conclusions. A good question is, was this paper critically reviewed before submitting it as bedrock evidence?

In all three cases, someone with a firm grip on the subject would have asked questions and pushed back before relying on these studies as major weapons in the RINs wars. Their weaknesses were exposed later, by others outside our industry with better and more comprehensive understanding of RIN fundamentals.

Conclusions

- The research relied upon by the refining industry in the RINs wars indicates weak understanding of RIN fundamentals.

- This weakness has contributed to the industry’s poor track record in the 8-year battle to get relief on RIN costs.

Recommendation

Considering the importance of RINs for profitability, every company affected by RINs should have at least one person with a deep and comprehensive understanding of RIN fundamentals including RIN pricing and economics.

Hoekstra Research Report 10

provides this kind of knowhow, plus our spreadsheet that applies a theoretical RINs pricing model developed by professors at University of Illinois and Harvard University, plus a full history of RIN prices, a summary of key events in RINs history, a full explanation of RIN price pass through theory and empirical studies, and a set of attachments that will make you a true expert on RINs pricing. It is available immediately to anyone at negligible cost. See our offer letter and contact me, or (better) just send a purchase order today. george.hoekstra@hoekstratrading.com +1 630 330-8159