Last week’s Part 2 of this series posed this question:

In terms of the pass-through question, how is the RIN tax situation (Figure 1) different than when a sales tax is imposed on finished gasoline?

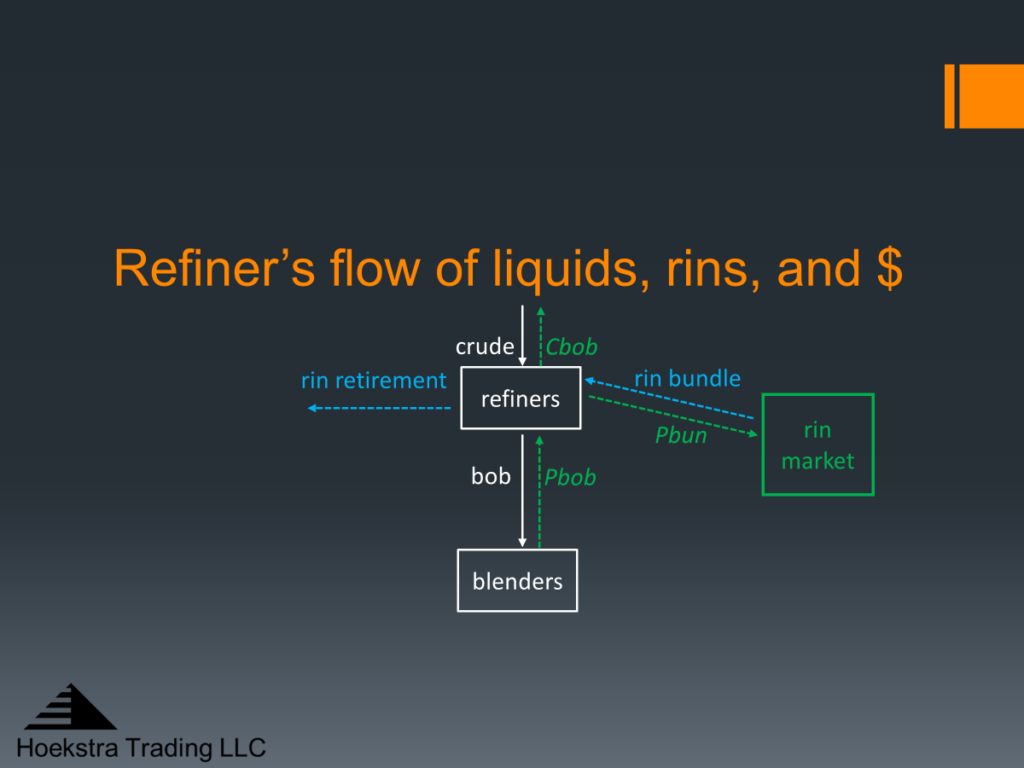

Figure 1 Flow of streams (white), RINs (blue) and dollars (green) in the market supplying bob to blenders

Contradictory views on this question are what drive a multi-billion dollar legal dispute now in its eleventh year with no end in sight. Camp A says the tax (Pbun) reduces refiners’ profit. Camp B says it doesn’t because the price (Pbob) received for the product (blendstock for oxygenate blending or bob) goes up by an offsetting amount, which is called the pass-through theory.

The view of Camp A in the dispute has been described in the following quotation that distills input from a large collection of stakeholders in Camp A:

“The degree to which the costs burdening small refineries will be passed through to the market depends on many factors, including the market power and the relative cost level of a small refiner relative to other market participants”

This statement is true in general but fails to differentiate between “costs” as a general category and the specific cost of the RIN tax. When a refinery incurs a large cost, like, for example, a maintenance cost that its competitors do not bear, that supplier-specific cost can obviously not be passed through to increase the market price because it is a supplier-specific cost. It will reduce that supplier’s profit. But when all suppliers in a market bear the same per gallon cost, like the RIN tax, or a sales tax, that cost will pass through, increasing the equilibrium market price of the product and offsetting the cost of the tax. The statement cited above therefore indicates a misunderstanding of what RIN cost passthrough means – it does not mean all costs pass through.

Also, the pass-through of the RIN tax to the market price does not require that any single supplier has market power. The market price emerges from the collective action of all participants in the market.

The above quotation continues:

“The cost for small refiners to comply with the RFS2 requirements can be substantial…. Their limited product slates coupled with an inability to blend renewable fuels means that many of the small refiners must enter the market to buy RINs.”

This statement is also true. But, again, it fails to recognize that all bob suppliers must acquire RINs, (not just small refiners), and, because they all bear the same per gallon RIN tax, that cost will pass through to the bob market price by the normal forces operating in a competitive market.

The statement also refers to small refiners’ limited product slates as factors. But limited product slates are not caused by the RIN tax obligation. Small refiners have many advantages and disadvantages compared to large refiners. They exist regardless of the RIN tax. And, because the RIN tax is the same per gallon amount for all obligated parties, its cost will pass through to the bob market price just like a sales tax does.

About small refiners’ inability to blend renewable fuels, that factor raises a different question, which is how does the RIN system affect others in the supply chain, like blenders, renewable feed suppliers, and blended fuel consumers who are not obligated parties. In fact, it raises a broader, more fundamental question which is where does the revenue from the RIN tax go? Referring again to the diagram in Figure 1, the only difference between it and a diagram for a sales tax is that the RIN tax goes to the “RIN market” instead of the government. What?? A tax whose revenue doesn’t go to government?? Then where does it go? That question is left for Part 4 of this series:

If the RIN tax revenue doesn’t go to the government, then where does it go?

Having tabled that (different) question for now, let’s return to today’s question about the RIN tax:

In terms of the pass-through question, how is the RIN tax situation (Figure 1) different than when a sales tax is imposed on finished gasoline?

The answer is there is no fundamental difference. Because they are both per gallon taxes that pass through to the markets they supply, they don’t affect the profits of those obligated to pay the tax. Contradictory contentions, like those cited above, have been addressed thoroughly and convincingly in favor of the pass through theory.

Conclusions

To obligated parties (suppliers of petro-fuels like bob), there is no fundamental difference between the RIN tax and a sales tax.

Both of these are taxes that pass through to the markets they supply, for the same reasons.

That is the answer to the pivotal question driving the 11-year, multi-billion dollar legal dispute that continues with no end in sight.

Hoekstra Trading clients use the ATTRACTOR spreadsheet to compare theoretical and market RIN prices, analyze departures from theoretical value, and identify trading opportunities on the premise RIN market prices will be attracted toward their fundamental economic values.

Get the Attractor spreadsheet, it is included with Hoekstra Research Report 10 and is available to anyone at negligible cost.