Phillips 66 3Q 2021 refining margin is still way low

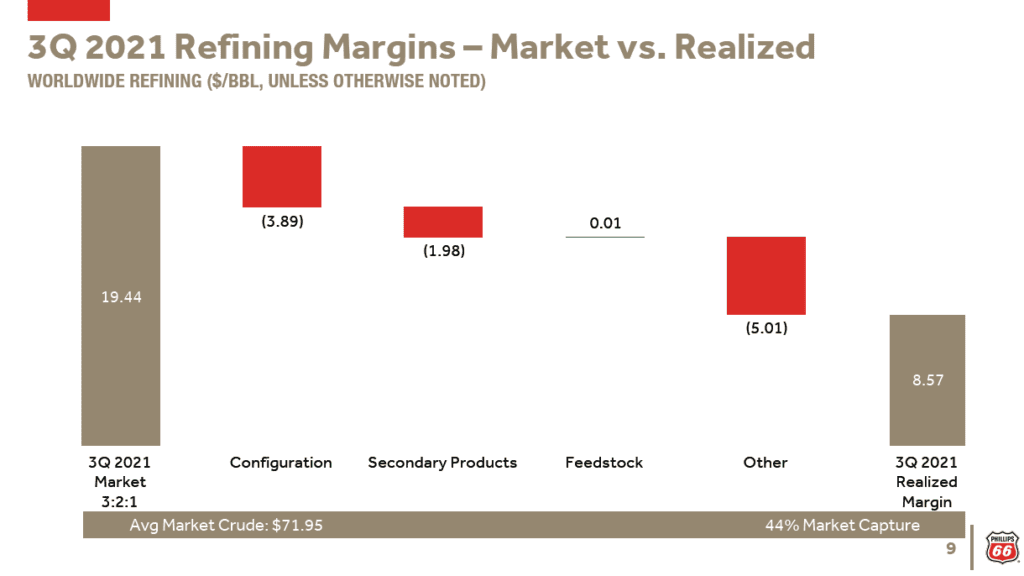

Today Phillips 66 (PSX) reported a realized refining margin of $8.57/barrel versus a market benchmark margin of $19.44/barrel. The ratio, called “market capture”, was $8.57/$19.44 or 44%: The data and calculation are shown nicely on this chart which PSX provides each quarter in their earnings conference call:

The $8.57 per barrel realized margin was an improvement over the second quarter’s $3.92 per barrel, but that $3.92 was inexplicably low and came in a quarter when the refining business segment lost $706 million. So some improvement was not only expected, but necessary.

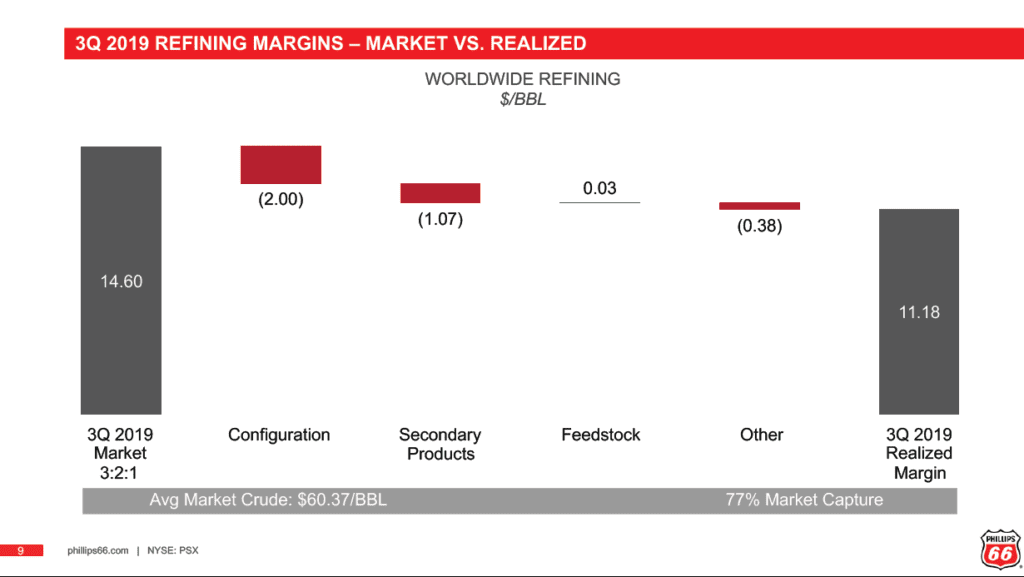

How does today’s 3rd quarter $8.57 realized margin compare to pre-lockdown norms? It is low. 2019’s 3rd quarter refining margin (we leave out lockdown year 2020) was $11.18 versus a market benchmark of $14.60, that’s 77% market capture:

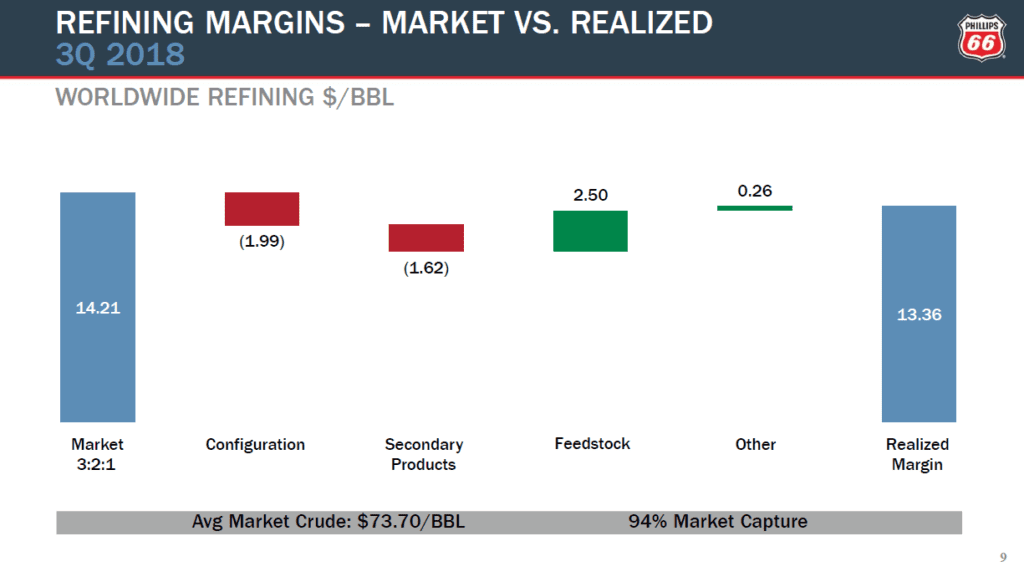

And the 3Q 2018 refining margin was $13.36 versus a market benchmark margin of $14.21, for 94% market capture.

Refining margin measures the difference in value of products sold (mostly fuels) minus the value of raw materials purchased (mostly crudes), and leaves out operating costs, selling costs and other costs that vary from quarter-to-quarter like depreciation and inventory adjustments. It is intended to be a pure measure of effectiveness in refining low cost crudes into high value fuels for sale in the lucrative US Tier 3 market, which is how the best-performing refiners are making money today.

PSX’s 3Q 2021 margin capture of 44% is still way low compared to the pre-lockdown norm.

Historically, the 3rd quarter delivers the highest refining margin of the year. PSX’s 3Q 2021 margin capture of 44% is still way low compared to the pre-lockdown 2018-2019 norm. My theory is this poor capture is caused by refining bottlenecks related to the new Tier 3 gasoline sulfur specification which make it difficult for many refineries to produce the low sulfur, high octane blend stocks needed to benefit from today’s lucrative US gasoline market. So instead of making those precious stocks from crude, they buy them, and/or export off-spec gasoline to lower-margin markets that don’t require Tier 3 spec gasoline, which are convenient but not very profitable ways to adapt.

Conclusion

- PSX’s 3Q 2021 refining margin of 44% is still way low compared to pre-lockdown norms.

- I attribute this to Tier-3 related refinery bottlenecks.

Recommendation

There are steps any refiner can take to immediately improve Tier 3 gasoline profitability. And there are many more things they could do in the near-term to turn Tier 3 from a problem into a profit opportunity. Refiners affected by Tier 3 should buy the Hoekstra Research Report 8 and use it to help take a fresh look at their Tier 3 strategy. The cost is negligible. For most refiners, it costs only about 1 minute’s worth of your annual revenue to immediately get your arms around this important, overlooked Tier 3 issue.

Hoekstra Research Report 8

Our three-year multi-client research project measured the effects of Tier 3 gasoline in pilot plant and commercial performance tests. We developed new methods and tools that helped our clients optimize performance of gasoline desulfurizers to avoid hidden hits to margin capture, and adopt profitable sulfur credit strategies. All our data and tools are available to anyone for immediate application at negligible cost. Please see this offer letter and join our client group today: Hoekstra-Trading-Offer-letter-Research-Report-8-refiners-under-1-MBD