RINatomy Part 2 – The RIN As A Tax

A Renewable Identification Number (RIN) is an environmental credit that is part of a price control system that manipulates the prices of fuel components to force otherwise non-economic biofuels into the US fuel supply.

Anatomy noun, anat·o·my ə-ˈna-tə-mē a study of the structure or inner workings of something

Read other blogs in this series RINatomy:

- Part 1 The RIN As A Subsidy

- Part 2 The RIN As A Tax

- Part 3 The RIN As A Mandate

- Part 4 The RIN As An Asset

- Part 5 The RIN As A Contingent Claim

In this price control system, the RIN works as:

- A subsidy

- A tax

- A mandate

- An asset

- A contingent claim

- An element of a nested structure

A tax

A familiar form of tax is a state sales tax on gasoline. The tax is imposed on the retail marketer. But we all know gasoline sales taxes are “passed through” by the retail marketer to its retail customers (us!), and, in effect, the tax ends up getting paid out of our pockets.

In fact, we are so conditioned by the pass through of sales taxes that we make the mental shortcut of thinking the sales tax is imposed on us customers. But that’s not technically true. The retail marketer actually pays the tax to the state. And if the state doesn’t get paid their cut, who does the state chase down to get it? It is the retail marketer, not us customers. So, technically, it is a tax on the retailer and the reason we end up “paying” it is because the retailer passes it through to us.

technically, the reason we end up “paying” the sales tax is because the retailer passes it through to us.

This technicality, about how a tax passes through the fuel supply chain, is the root issue underlying a 10-year, one hundred million dollar legal battle over RINs that is not yet resolved (see SRE = Sustained Revenue for Expensive lawyers).

The RIN tax

Similar to a state sales tax, the RIN’s Renewable Volume Obligation (RVO) functions as a tax on petroleum-based diesel and gasoline supplied to the U.S. market. It is imposed on refiners and importers of road transportation fuels derived from crude oil.

This raises the question whether, like a sales tax, the RIN tax passes through the supply chain from the refiner (who actually pays the tax) to those downstream, like the terminal who stores fuels in bulk tanks, the blender who blends refined petro-fuel with ethanol, the distributor who trucks blended gasoline to the station, the retailer who sells the finished fuel to us, and eventually to us consumers.

The prickster tax

In Illinois, a state governed by J. B. Pritzker, a gasoline retailer pays a 45 cent per gallon state sales tax on gasoline sold at retail, and that sales tax passes through fully to us motorists via a higher market price we pay at the pump (I nick-named this tax the prickster tax).

Imagine you are an Illinois retail station owner who decides NOT to pass through the state gasoline sales tax. Your price would then be lower than the competitors’ market price by 45 cents per gallon. You would attract and fill up long lines of cars, and then, when Governor Pritzker chased you down for his 45 cent cut on every gallon you sold, you would go broke.

Suppose instead you decide, as a promotion, to pass through just 90% of the sales tax instead of 100% as your competitors are doing. Your price would then be 4.5 cents per gallon lower than the competitors’ market price. You would attract some sales volume from competitors, who may then match your lower price to regain their market share, starting a price war.

In that price war, some weak suppliers may face being forced out of the market because their profit will go negative if they reduce their price by 4.5 cents per gallon. In a desperate attempt to stay in business, the weakest competitors might keep their price at the original (higher) market price which would be a counter-force pushing your discounted price back up.

Eventually, as market shares and price fluctuate, things would re-equilibrate, probably near where they are today, where every retailer passes through its 45 cent per gallon cost for the tax.

Systemic cost

The point of this thought experiment is to illustrate how, in a competitive market, a state sales tax, imposed on all retailers equally, will pass through to retail customers.

More generally, in a fully competitive market, a systemic cost increase that affects all competing suppliers equally will be pushed, by competitive pressures, down the supply chain to the next level of competition.

In a fully competitive market, a systemic cost increase that affects all competing suppliers equally will be pushed, by competitive pressures, down the supply chain to the next level of competition.

In analyzing the pass through of the RIN tax, we can refer to this familiar sales tax analogy and make use of two key criteria for full pass through, that the cost must be systemic (affecting all suppliers equally), and the market must be competitive at that level of competition.

The pass through theory, in addition to being controversial, plays an essential role in RIN pricing and economics. In fact, we will see that, if pass through does not occur, the RIN price control system will fail.

if pass through does not occur, the RIN price control system will fail.

RINatomy

So far this blog series has covered the RIN as a subsidy that draws otherwise non-economic renewable fuels into the fuel system, and the RIN as a tax on refined fuels. Next we will cover the RIN’s role as a mandate.

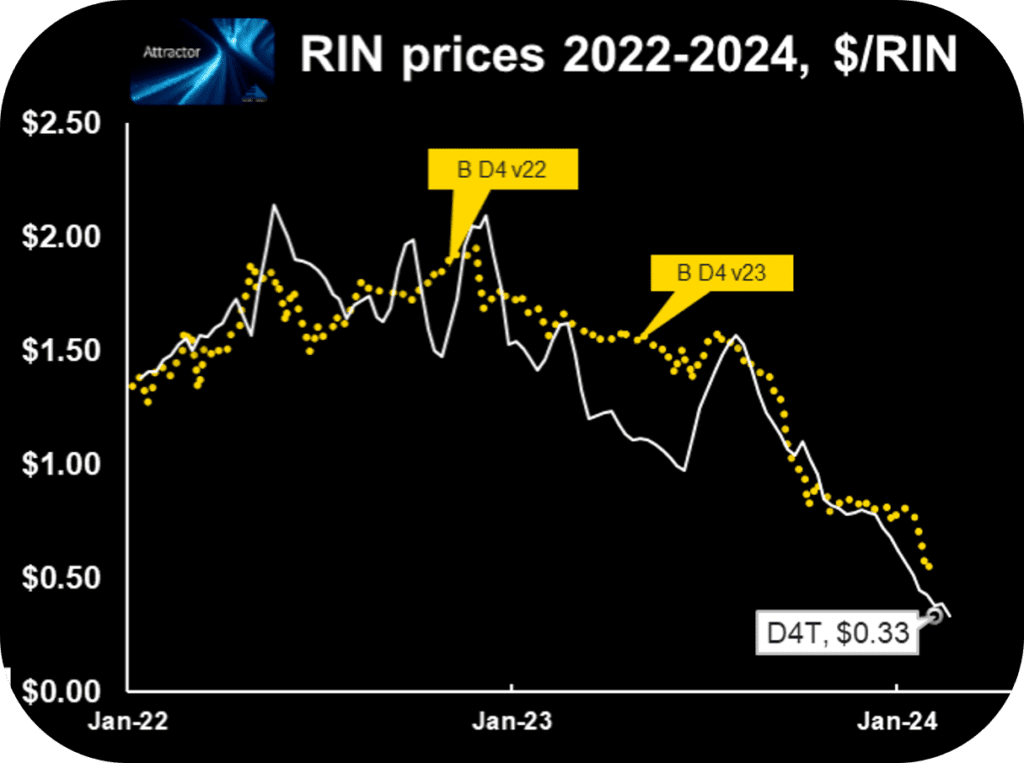

This series, titled RINatomy, covers the basic structure and inner workings of the RIN price control system, something I learned about 3 years ago that helped me and Hoekstra Trading’s clients get a grip on what drives the otherwise bewildering behavior of RIN prices, and to then effectively track, interpret, and anticipate RIN price behavior using the Attractor spreadsheet which compares D4 RIN market prices to a theoretical value called D4T which is calculated using economic fundamental and is the world’s first licensed theoretical value of an environmental credit.

Attractor update

The Attractor spreadsheet shows the D4 RIN market price (gold points) and the “D4T” theoretical value (white line and open white data point) updated through last Friday. The theoretical value of a hypothetical D4 RIN with 1 year remaining life (“D4T”) is $0.33 which is down 11 cents from last week.

Hoekstra Trading clients use this spreadsheet to compare theoretical and market prices, analyze departures from theoretical value, and identify trading opportunities on the premise RIN market prices will be attracted toward their fundamental economic values.

Get the Attractor spreadsheet, it is included with Hoekstra Research Report 10 and is available to anyone at negligible cost!

George Hoekstra george.hoekstra@hoekstratrading.com +1 630 330-8159