A billion dollar question: do refiners recapture RINs expense?

There is much confusion in the refining industry on whether and how $billions/year of Renewable Identification Number (RIN) expenses are being passed through and recaptured by refiners in their profit margins.

The issue has been around for many years and re-surfaces during run-ups in RIN prices.

For example, in the Phillips 66 first quarter 2021 earnings conference call, four financial analysts raised the question:

The questions

Roger Read – Wells Fargo Securities

I was just curious how the elevated RINs issue is running through the business? . . . I just wanted to make sure that you all are more or less balanced on the RIN issue and maybe how you think about that if it maintains these elevated levels kind of hits the rest of the year on capture for refining?

Jason Gabelman – Cowen and Company

I‘m just trying to understand the ability to pass through the RIN cost to the consumer within your marketing business. And what I’m thinking is, does the net RIN cost of fill-ups go up during periods of weak demand like during COVID, just because it’s more difficult to pass through the cost to the customer?

Doug Leggate – Bank of America Merrill Lynch

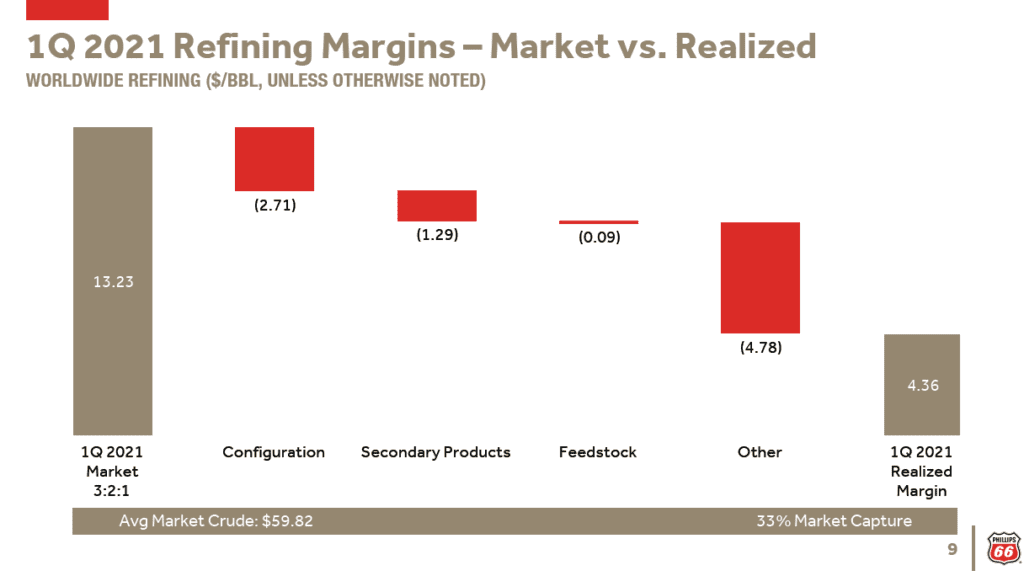

Referring to the fourth red bar in this slide which shows a $4.78 hit to refining margin in the “other” category, Doug Leggate asked:

It was $4.78 this quarter. The past 3 or 4 quarters it started at negative $2.22. Back in 2019, the average is around $0.30, $0.40 negative. And it seems that, that number has moved up almost lockstep with the RIN. . . . what’s going on here? Is that the biggest driver of that delta? And what should we be thinking on a go-forward basis because it’s obviously denting the capture rate quite a bit.

and,

Even if I look elsewhere in the business, whether marketing or whatever, I can’t see where you’re getting that back. So can I just ask you again to clarify when is it (RINs) a net neutral or negative for Phillips?

Paul Cheng – Scotiabank, referring to the statement that Phillips 66 blends about 50% of their fuels:

50%? That seems really low, given how big is your total network in the U.S. So are we missing something here?

The analysts are hungry for answers. “What’s going on here? Are we missing something? What should we be thinking on a go forward basis?” They want some clarity from the C-Suite on how rising RIN prices are affecting refining profitability.

The answers

Robert Herman – Executive Vice President, Refining:

We believed and continue to believe that the RIN is priced out in the crack.

and:

Some of it we get through our own liquid blending at our terminals, right, and generate the RINs there for our needs, and it really does pass on downstream to the ultimate consumer.

Greg Garland – Chief Executive Officer:

We blend about half. So we generate about half the RINs we need for our obligation at Phillips 66.

Mark Lashier – President and Chief Operating Officer:

It’s a direct hit to the capture rate. So as the RIN pricing increases, you’ll see that happening there.

Robert Hermann – Executive Vice President Refining:

At the end of the day, as Brian covered earlier, we blend for about half and then half is other people blending and we’re exposed to the commercial market on those RINs. So net-net, it is a negative to us at the end of the day. We do not capture the RIN at the 100% level.

Analysis

The above answers didn’t clarify much. Which is it?

It is priced out in the crack – this suggests RIN costs are fully recaptured in margins.

We blend about half. So we generate about half the RINs we need for our obligation – this ignores the other half, which is the half that’s in question.

It’s a direct hit to the capture rate – this suggests a dollar-for dollar hit to margin.

Net-net, it is a negative to us at the end of the day. We do not capture the RIN at the 100% level – this describes a muddled middle ground.

In fact, on examining these answers, thoughtful investors would conclude the C-suites themselves are unclear on the issue.

Economic theory says that, in fully competitive markets, when RIN prices increase, the prices of petroleum fuels adjust at wholesale and retail levels to new equilibrium values that reflect refiners’ increased RIN expenses. This theory is supported by widely-publicized empirical studies. It points to the first answer, which says that RIN cost is “priced out in the crack”, even for merchant refiners.

By this theory, whether or not a refiner is blending renewable fuels, he is recapturing increased RIN expenses in the form of increased market prices for his petroleum fuels. And by this theory, the increased RIN expense is being offset by higher realization on petroleum fuels, that is, higher realization than would be otherwise.

Conclusion

The evidence is conclusive that retail and large wholesale fuel markets are fully competitive and that, in those markets, increased RIN expenses are being recaptured in higher realized refining margins.

What about smaller local wholesale markets — are they fully competitive, such that increase RIN expenses are fully recaptured? To my knowledge, that has not been proven. But even if they are not, healthy refiners can recapture increased RIN expense through proactive use of their pricing power in those markets.

The upshot is that it is not legitimate to blame shrinking margin capture rates on RIN expenses.

And it follows that other factors are contributing to the shrinkage in refiners’ realized margin capture.

Recommendations

Refining executives should demand a full understanding of how they are recapturing RIN expenses in wholesale margins. They should not be satisfied until they personally have a firm grip on the justification for that claim.

Refining executives should demand a full understanding of the other factors contributing to shrinking margin capture rates.

George Hoekstra

Anyone with a stake in RINs pricing and economics should get Hoekstra Research Report 10 which includes the Hoekstra ATTRACTOR spreadsheet spreadsheet that accurately calculates D4T, the theoretical RIN price, tracks it versus quoted market prices, and predicts how RIN prices will change with the variables that affect them. Why not send a purchase order today?

George Hoekstra george.hoekstra@hoekstratrading.com +1 630 330-8159

Anyone with a stake in RINs pricing and economics should get Hoekstra Research Report 10