An update on the MPC-PSX stock price spread

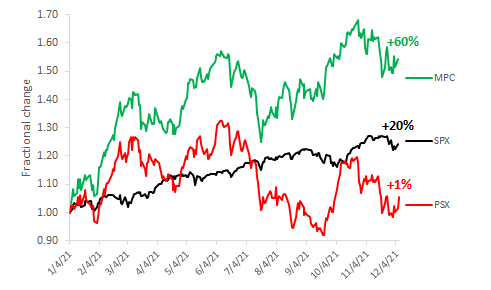

Six weeks ago, this comparison of Marathon Petroleum Corp (MPC – green) and Phillips 66 (PSX -red) 2021 stock price performance highlighted a striking difference:

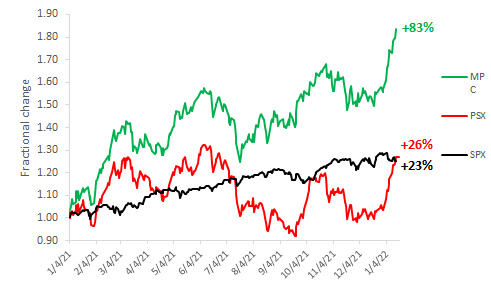

Since then, oil stocks have surged. Here is how the same chart looks six weeks later

MPC and PSX have both increased 20%, relative to the base point on the first trading day of 2021 while the S&P 500 is unchanged. So the six-week surge hasn’t changed the big spread between MPC and PSX which remains 60%.

My Theory

I believe Marathon’s refineries are highly advantaged compared to Phillips’ in their ability to capture the high gasoline margins available in the US market today, and this is related to the new Tier 3 ultra-low sulfur gasoline specification that just kicked in this year, and this is gradually being recognized in the reported refining margins and the stock prices, and this is the main cause of this Big Spread that started forming in early-2021.

This theory is not popular among refining higher-ups or financial analysts, in fact you will not find it mentioned anywhere but here. If Tier 3’s impact on profitability interests you, you should read several previous posts like this, and keep watching this blog.

Year-end earnings reports are just around the corner. If I were a financial analyst representing investors, with access to the PSX C-Suite, I would ask two questions:

- What is the root cause of your bottom-quintile margin capture on fuels in 2021?

- What specific steps have you taken to improve it in 2022?

I see no indication PSX plans to use any of their $1.9 billion capital spend in 2022 to improve gasoline margin. So maybe I am wrong. But if I am right, the spread will widen, so I remain long the MPC-PSX spread.

Recommendation

There are steps any refiner can take to immediately improve Tier 3 gasoline profitability. There are many more things they could do in the near-term to turn Tier 3 from a problem into a profit opportunity. Refiners affected by Tier 3 should buy the Hoekstra Research Report 8 and use it to help take a fresh look at their Tier 3 strategy. The cost is negligible. For most refiners, it costs only 1 minute’s worth of your annual revenue to confront and get your arms around this important, overlooked Tier 3 issue.

Hoekstra Research Report 8

Our three-year multi-client research project measured the effects of making Tier 3 gasoline in pilot plant tests and in sixteen commercial gasoline desulfurizers. We developed new methods and tools that are helping our clients optimize performance of gasoline desulfurizers to avoid hidden hits to margin capture and adopt profitable sulfur credit strategies. All our data and tools are available to anyone for immediate application at negligible cost. Please see this offer letter and join our client group today: Hoekstra-Trading-Offer-letter-Research-Report-8-refiners-under-1-MBD