RIN Price Nosedive Part 1 – C-Suites Questioned On RIN Price Nosedive

Last week financial analysts asked refining executives about the nosedive in the D4 Renewable Identification number (RIN). From responses to this week’s questioning:

- There is no evidence refining executives anticipated the 3rd quarter D4 RIN price nosedive

- Explanations of the cause of the D4 RIN price nosedive are weak

- There is no basis for investor confidence in refiners’ forecasts of RIN prices.

Read more blogs in this series, RIN Price Nosedive:

- Part 1 C-Suites Questioned On RIN Price Nosedive

- Part 2 Was It Foreseen, What Was The Cause, Will It Continue?

- Part 3 It Was Foreseen, It’s Cause Was Competition, And it Will Continue

- Part 4 A Nosedive Is One Thing, A Cliff Is Another

- Part 5 Dissecting the 2023 RIN Price Nosedive

Below are 3 excerpts, from Neste and Valero’s 3rd quarter earnings conference calls:

1. Question from Peter Low, Financial analyst, Redburn Atlantic

Hi, thanks. Yes it’s one just on the D4 RIN. We’ve seen prices fall significantly in October. My understanding is that it is an important component of value for RD in the US. Yet your 4Q margin guidance remains at a very high level despite the fact that you’ve got an increasing share of volumes being sold in the US. So could you perhaps talk a little bit about to what extent your profitability is tied to the RIN? And what impact if any the recent fall could have? That would be helpful.

From Neste Oyj 3rd quarter 2023 earnings conference call, Oct. 26, 2023

Answer from Carl Nyberg, Neste Oyj Executive Vice President, Renewables

Thanks, Peter. So Carl here, I’ll take the fourth question first. So indeed we have seen a steep decline in the RIN values. However I mean we do hedge part of our RIN exposure. And on that basis we are now guiding also the Q4 margin accordingly. So we have taken into account the change that we saw in the market here. Now, I think it’s also very important to take into account when we talk about the RIN that’s one piece of the puzzle here. And of course the feedstocks like I mentioned also have been now reacting to this. So, we do believe that the RIN value needs to work in relation to the feedstock markets as well as to the heating oil prices. So, in that sense it’s just one component here and we need to look at the full picture. But indeed this decline here has been taken into account. And part of that exposure is managed through our hedging activities.

From Neste Oyj 3rd quarter 2023 earnings conference call, Oct. 26, 2023

2. Question from Kate Sullivan, Citi

Hi. Thanks for taking my questions. Firstly a follow-up on the RINs question. You’ve talked about your RIN hedging into 4Q. But going into 2024, how do you see the RIN dynamics impacting your renewable product sales margin considering the renewable volume obligation has been set up to 2025 and US supply is increasing. It doesn’t seem that RIN pricing is going to get tighter in light of that supply and dynamic.

From Neste Oyj 3rd quarter 2023 earnings conference call, Oct. 26, 2023

Answer from Carl Nyberg, Neste Oyj Executive Vice President, Renewables

Carl here. Maybe I’ll start with your first question around the RIN development. And indeed I mean we – as mentioned earlier, so we have hedged part of our RIN exposure in Q4. We also have hedged some volumes in 2024. But obviously, we have a large exposure to the RIN prices. And in that sense that is – that will change when we go into 2024. On the other hand, as mentioned earlier, we have to look at this as a package. The RIN values need to reflect also the other values that we are seeing. So I think that the fundamentals around RIN has typically been derived from the biodiesel margins. And we do believe that that will remain a key. So in that light, I would say that sort of we will see a new market stabilizing around a new level and return to some kind of equilibrium. I do have to say as well at the same time that having the feedstock flexibility capabilities will be a very important part also in driving value creation and margins in the US markets going forward. And we believe that this will be an important way for us also to create great value.

From Neste Oyj 3rd quarter 2023 earnings conference call, Oct. 26, 2023

3. Question from Ryan Todd, financial analyst, Piper Sandler:

Could you talk through a little bit about what you’re seeing in renewable diesel markets? 2Q margins were obviously quite soft and indicators been weak. Was there any impact from hedging losses in the quarter and, if there were, kind of a rough estimate of maybe what that was? And then can you just more broadly talk about what you’re seeing in terms of supply demand in the marketplace, impact of RIN pricing and RVO limitations, et cetera?

From Valero Energy Corp. 3rd quarter 2023 earnings conference call, Oct. 26, 2023

Answer from Eric Fisher, Valero Senior Vice President-Product Supply & Trading and Wholesale

Sure, Ryan, this is Eric. I think we saw the RIN prices drop pretty quickly kind of in that September and into October. And really, as you stare at that drop, it was kind of on the news that there was the anticipation of a couple of big start-ups at the end of the year that have now been delayed. It was also in the news that, with Russia freezing out its exports that it would force the U.S. to export more, therefore, drop the obligation. So the combination of all that news kind of caused a precipitous drop in the RINs kind of right at the end of the quarter and into the beginning of the fourth quarter. The real margin loss there is really because as fat prices have since adjusted in the spot market but obviously, there’s a lag of our fat prices that kind of carried on that have since started to catch up with this drop in credit prices. But we’ll see that continue to carry through, through the fourth quarter.

From Valero Energy Corp. 3rd quarter 2023 earnings conference call, Oct. 26, 2023

Conclusions:

From these and other responses to this week’s questioning:

- There is no evidence refining executives anticipated the 3rd quarter D4 RIN price nosedive

- Explanations of the cause of the D4 RIN price nosedive are weak

- There is no basis for investor confidence in refiners’ forecasts of RIN prices.

Recommendation

Those with a stake in RINs pricing and economics should get Hoekstra Research Report 10 which includes this Hoekstra IMS RINs pricing spreadsheet that accurately calculates theoretical RIN prices, tracks them versus actual prices, predicts how RIN prices will change with the variables that affect them, and includes 6 months of unlimited consultation by phone and E-mail. Here’s the offer letter including the Table of Contents and a sample invoice with all the information needed to prepare a purchase order. Why not send a purchase order today?

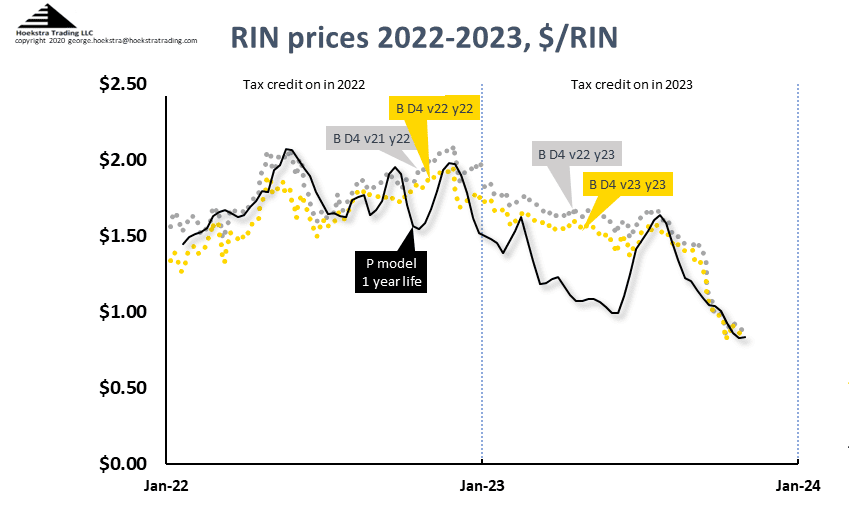

The chart below shows the Hoekstra IMS RINs pricing spreadsheet with D4 RIN market price (gold and silver points) and the theoretical D4 RIN value calculated by Hoekstra Trading’s application of the Irwin-McCormack-Stock (IMS) RIN price model (black line) updated through last Friday. The theoretical value of a hypothetical D4 RIN with 1 year remaining life is $0.84.

Hoekstra Trading clients use this to compare actual to theoretical prices, analyze market price departures from theoretical value, and identify RIN trading opportunities on the premise RIN market prices will be attracted toward their fundamental economic values.

George Hoekstra george.hoekstra@hoekstratrading.com +1 630 330-8159