CVR Energy – another case study in low refining margins

Investors and analysts are confused about how to interpret low refining margins being reported this year. Much of the confusion stems from the confusing topic of RINs.

I believe the low margins indicate a more fundamental weakness in the performance of many US refineries, which is inability to make enough on-spec gasoline from crude; and that weakness was triggered by the Tier 3 ultra-low sulfur gasoline specification that just kicked in this year.

The wet margin squeeze

To make a profit, sales revenues must exceed the cost of raw materials. That difference is the most basic starting margin from which all costs, like operating expense, sales expense, and RINs must be paid.

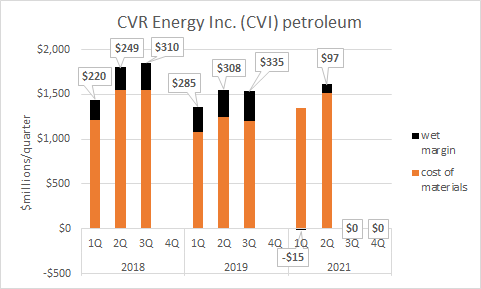

On this chart, the total height of each bar is quarterly sales revenue. The orange segment is that quarter’s cost of raw materials (mostly crude). The black segment and data label show the difference between revenue and cost of raw materials. This chart is for CVR Energy Inc.’s Refining business segment. The COVID lock-down year, 2020 is omitted.

The six left-most black bars show CVR Refining’s revenue minus raw materials cost during 2018-2019 was $300+/-50 million per quarter. The two right-most bars show it’s been $40+/-60 million so far in 2021.

What is the cause of this shrinkage in the black bar? It’s not RINs — RIN cost is nowhere in this data. It’s not market conditions — crack spreads were $18+/-2 per barrel in all these quarters. It’s not throughput — CVR’s throughput was 210,000+/-20,000 barrels/day across the quarters shown here.

Only two things affect the black bar — the revenue from product sales and the cost of feedstocks.

I can’t find a formal name for the metric shown by the black bar. It is a component, but only one component, of gross margin. For convenience, I will hereby call the black bar the “wet margin” because it depends only on the volumes and qualities of wet barrels flowing into and out of the refinery.

Could the wet margin squeeze shown in the chart be a COVID lock-down hangover effect? Perhaps. But my theory is that CVR, like many others, is having difficulty making enough low sulfur, high octane blend stocks from crude to fully capitalize on the high gasoline margins available in the market today, and that difficulty has been triggered by the Tier 3 ultra-low sulfur gasoline specification which just kicked in this year.

Tier 3 adaptations

With Tier 3, all gasoline sold in the USA must be 10 ppm sulfur which is much more difficult to make than the 30 ppm gasoline made before. Facing this new difficulty, refiners (not only CVR) are making changes to adapt to new sulfur and octane-related bottlenecks triggered by Tier 3. But those adaptations are costly. Here are some that fit in the categories of purchasing, downgrading, or restricting things:

Purchasing, downgrading, and restricting things reduces the value of the product slate and/or increases the cost of feedstocks.

My conjecture is that CVR and other refiners are purchasing barrels of something more expensive than crude, like low sulfur feedstocks or gasoline blend stocks, to facilitate making 10 ppm sulfur gasoline. That would inflate the raw materials cost for the same product slate and squeeze the wet margin, just like we see on the chart.

If you’re going to pay all costs out of a starting margin that’s shrunk by a factor of 7, that will be difficult even before factoring in RINs.

That’s my theory on the wet margin squeeze. It is certainly a contrarian theory — but a very well-informed contrarian theory supported by lots of hard data.

Investors should learn the answer to this question which I have been asking refiners: to what extent is Tier 3 a factor in the 2021 wet margin squeeze? If the squeeze is a lock-down hangover, I suppose it will go away on its own. But if it’s a Tier 3 effect, it will persist until action is taken.

Most refiners deny Tier 3 is affecting their profit, or remain mute on the question. I think the question can be answered without bringing up the confusing topic of RINs. And if you’re going to continue paying all costs out of a starting margin that’s shrunk by a factor of 7, that will be difficult even before factoring in RINs.

Conclusions

- CVR Refining’s wet margin in 2021 is lower than the pre-lock-down period by a factor of 7.

- My conjuncture is this indicates a fundamental weakness in ability to make Tier 3 gasoline from crude.

- This weakness exists in many North American refineries.

- Investors should learn the extent to which Tier 3 is a factor in the wet margin squeeze.

Recommendations

There are steps any refiner can take to immediately improve Tier 3 gasoline profitability. And there are many more things they could do in the near-term to turn Tier 3 from a problem into a profit opportunity. Refiners affected by Tier 3 should buy the Hoekstra Research Report 8 and use it to help take a fresh look at their Tier 3 strategy. The cost is negligible. For most refiners, it costs only about 1 minute’s worth of your annual revenue to immediately get your arms around this important, overlooked issue.

Hoekstra Research Report 8

In a 3-year, $1 million research project, our client group gathered new data, developed new methods and new tools to help refiners avoid hidden pitfalls and improve profitability of Tier 3 gasoline. All our data and tools are available to anyone for immediate application at negligible cost. All refiners affected by Tier 3 should have it. Just see this offer letter and join our client group by sending a purchase order today: Hoekstra-Trading-Offer-letter-Research-Report-8-refiners-under 1 million barrels/day