RINs and sulfur credits – where do the $billions go?

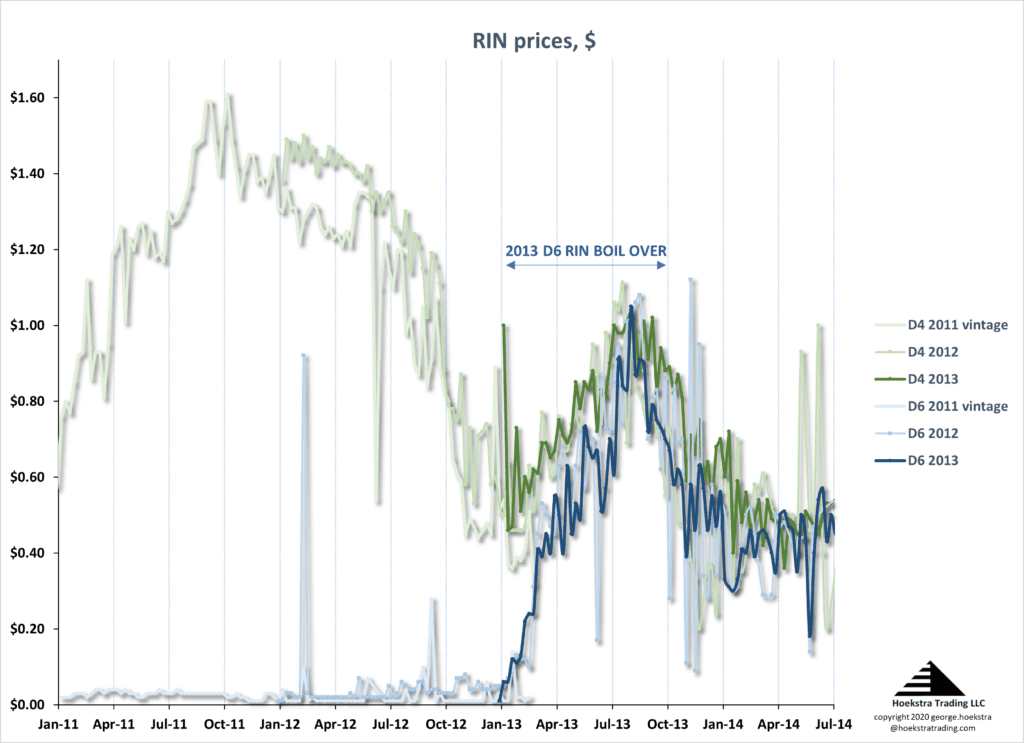

In 2013, the price of D6 Renewable Identification Numbers (RINs) skyrocketed sixty-fold (not sixty percent!) in weeks, triggering a financial crisis that rocked the US refining industry and is still making news today:

The bright colored data shows the 2013-vintage D6 RIN (blue) price snapping up to a new relationship with the D4 RIN (green) in the first quarter of 2013. For an explanation of this chart, please download the article RINs and sulfur credit pricing and economics and read our previous blog post RINs and sulfur credit pricing and economics — a follow-up.

Refiners have been paying $billions/year in RIN expenses since 2013. Where do all those billions go?

With most government programs, like speed limits and parking meters, compliance failures result in fines that go to the government. But with RINs and sulfur credits, compliance failures result in payments to other market participants, meaning there are losers and winners!

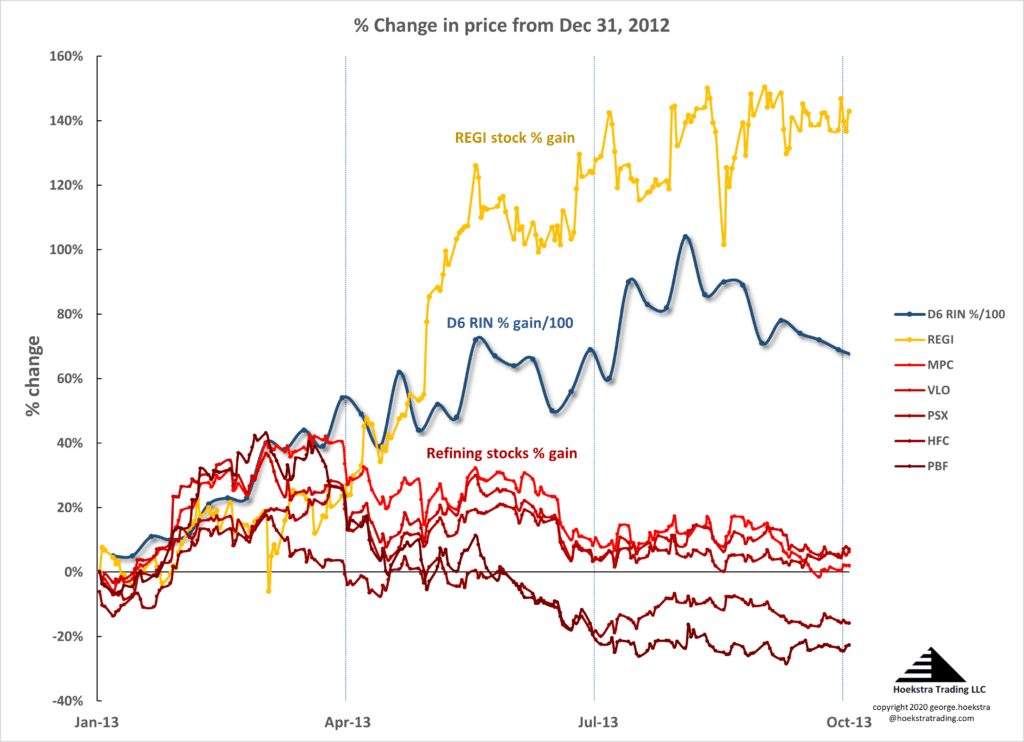

Renewable Energy Group (REGI)

For example, among recipients of 2013 RINs payments was Renewable Energy Group Inc. (REGI), a biofuels producer whose stock price (gold) soared while refining companies’ sank:

The (blue) % gain in RIN price is divided by 100 here to fit it on the same chart with stock returns.

2013 earnings call transcripts confirm that this contrast in stock price patterns is explained by RIN cash transfers from refiners to REGI. RINs are a central element of REGI’s profitability. Their deep and broad understanding of RIN economics enables them to maximize the benefit of changing RINs prices for their business and their shareholders.

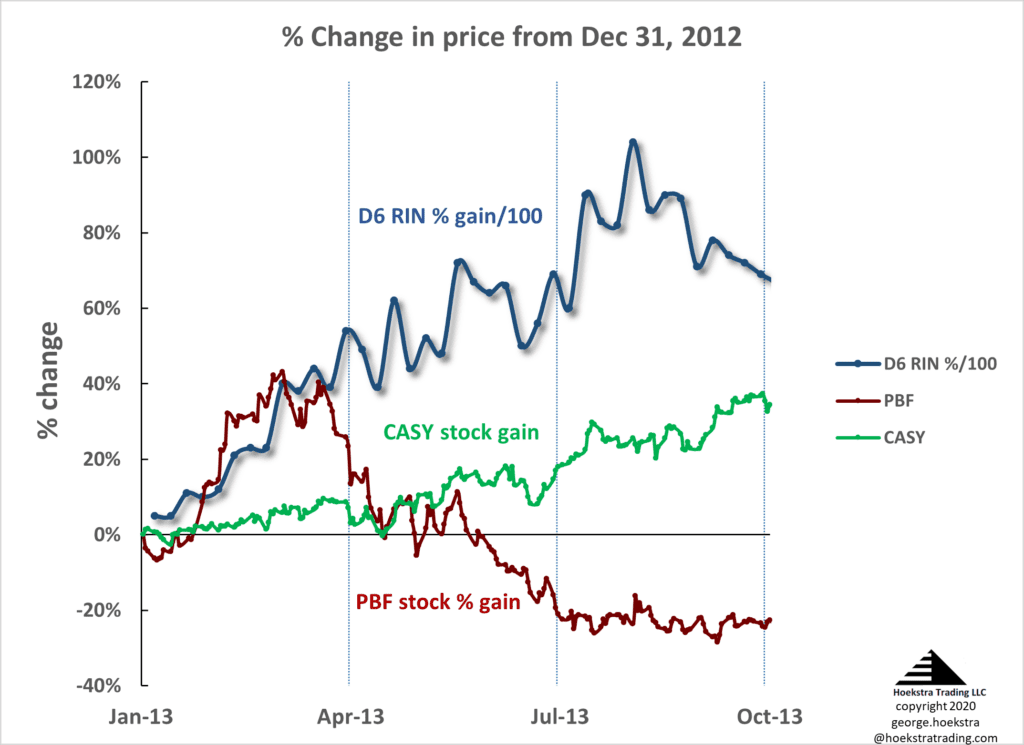

Casey’s General Stores (CASY)

Another beneficiary was Casey’s General Stores (CASY). Casey’s is a chain of fuel and convenience stores in the midwest and southern United States whose stock price (green) rose 40% in 2013 and resembles a mirror image of PBF:

In 2008, Casey’s developed an internal RIN accounting and processing system that interfaced seamlessly with EPA’s system. This capability had run smoothly for years, even when RINs weren’t generating significant profits.

But when the D6 RIN price suddenly popped its cork in 2013, a new revenue stream popped up onto Casey’s computer screens.

With full awareness of the RINs markets, Casey’s executives immediately directed sales incentive programs into regions where they were generating RINs, to maximize RIN generation and gasoline market share in those regions, which now effectively provided opportunity for a higher fuel margin, at the expense of less RIN-aware competitors. RINs revenue delivered, directly, a 30% increase in net income which contributed to the 40% increase in share price shown on the chart.

Tier 3 gasoline

With RINs, by design, refiners are playing against a stacked deck because the program was engineered to subsidize growth of renewable fuels at the expense of fossil fuels suppliers.

That is not true with Tier 3 gasoline.

Like RINs, Tier 3 credit payments will add up to $billions in cash transfers that will go to other market players, not the government, when the Tier 3 market matures. But, unlike RINs, there is no government-imposed stacking of the deck to favor a new fuel industry. Winners and losers will be determined in a fair game among businesses competing in the production and delivery of ultra-low sulfur gasoline and octane to the US market.

It is a new game, and big opportunity for North American refiners. Some of them will almost surely be big winners.

Anticipating Tier 3

As always, refining executives are dealing today with important and urgent issues (like safety, reliability, turnarounds, and survival!). The industry is shedding thousands of people and internal planning capabilities are not what they were.

No longer can every refiner have its own proprietary expertise on everything. For those who don’t, it’s increasingly valuable to use focused, third-party research which is readily available and underutilized by refiners who have been accustomed to going it alone.

Tier 3 is a known coming risk. Our client group has used shared resources and external networks to dig deep, get critical data, and develop thorough understanding to enable early, well-informed decisions.

None of our Tier 3 research is proprietary. Our multi-client reports are available immediately to anyone at negligible cost.

George Hoekstra +1 630 330-8159 george.hoekstra@hoekstratrading.com